In this first article, Sebastian Moritz, Director of MORICON, will look at ways to meet rental demand in the UK, explain what causes the undersupply, and highlight possible solutions.

MORICON Consultants shares thoughts on the Build to Rent market in the UK over a series of 5 short articles. The topic was part of the IRPM Build to Rent Level 4 course assignment and reflects only the authors’ opinions.

In February 2017, the British Property Federation published a widely reviewed report on unlocking the benefits and potential of BTR (Build to Rent) for the UK Housing market[2]. The paper highlighted a range of measures undertaken by the government, local authorities, and the private sector to ensure steady growth in the housing market in support of the failing house-building targets.

In 2020, the BPF (British Property Federation) reported that 43,236 units are complete, 33,505 are under construction, and 80,771 are in planning, for a total of 157,512 units[1] – well short of the envisioned target of 200,000 units.

As expected with such a complicated problem, several factors contribute to the lack of supply and subsequently impact the overall rental demand in the UK; the main ones are listed below:

Many operators feel that the Local Authorities (Local Authority) play a significant role in aggravating the situation, as most Local Authorities are reliant on a few framework policy documents – set out in the National Planning Policy Framework (NPPF)[3]. The National Planning Policy Guidance (NPPG)[4] lacks concise policies assisting them with BTR. Currently, the framework still favours owner-occupiers and affordable housing – and both models differ from BTR, and more education and explanations are required.

Another issue lies in applying tenure-blind space requirements via Local Authorities: the mandatory – and sometimes ill-informed planning for the unit mix and size can result in missed opportunities for additional space. Three- or four-bedroom units are not generally required for a BTR property. However, this is driven by the Strategic Housing Market Assessment without considering the type of tenure for which this building is designed.

Size matters: many BTR properties have additional amenities as part of the expected offering– to offset higher construction costs. Due to this, more units need to be built, which can be challenging with the limited space. To encourage developers to plan more BTR properties, the standard size of the units could be revisited, and the achieved extra space utilised for further units – preferably on a discounted market rent (DMR) scheme.

Once planning has been completed, the building process can be hindered by the long mobilisation periods granted – in England, this is currently three years[5]. In the worst case, a site can lie dormant for three years until construction starts or before consent can be withdrawn. This, paired with a phased construction, will reduce the available units in the short term without a reliable supply pipeline.

The phasing of development – though perfectly legal – aims to avoid a sudden surplus of units but artificially fuels undersupply and growth of land value and house prices. Construction considerations and practicalities in site management mostly lead it. Recently, the Local Government Association claimed that only 60% of all permitted buildings have been built, and the issue lies with both – the regulator and developers.[6]

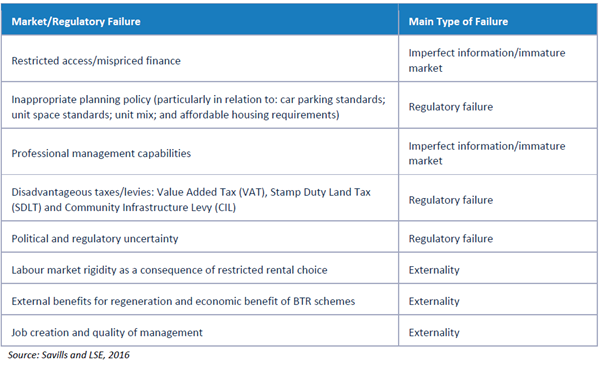

The following table[7] highlights the variety of market & regulatory shortcomings that have an impact on the BTR sector:

Whilst job creation schemes, labour markets or external benefits for regeneration have no direct impact on BTR schemes, a range of “home-made” issues need resolution. Extra costs, such as VAT and Community Infrastructure Levy (CIL), are some of the regulations that require review, as those extra costs hit the viability calculations of a project and can deter a developer from building a BTR project.

To overcome the planning hurdle and avoid alienating the Local Authority’s planning committee, I advocate the formation of partnerships between Local Authorities and Housing Associations wherever possible.

This helps to alleviate misconceptions and closes knowledge gaps while helping to smoothen out the planning process[8]:

Educating the local authorities on the differences between BTL and BTR schemes could lead to a better understanding of the issues with current planning. This approach could result in a different view on space requirements at the planning stage and soften Local Authorities’ stance regarding slightly smaller DMR units rather than a fixed set of affordable units as demanded in housing strategies.

Another way to increase stock could be to concentrate more on Permitted Development Rights (PDR), as seen at the very successful Office-to-Residential Conversion at the Boulevard Crawley by Platform: the change resulted in an extra 27 units above the borough’s space standards – which boosted the profitability of the development as well.[9]

Modular construction techniques or timber frame construction should be reviewed to shorten the construction period and maintain profitable development – this would lower costs and increase sustainability.

Developers could prepare the full spectrum of qualifying mobilisation works[10] as soon as new sites are going into the planning cycle, triggering the building process, whilst separately working on a range of out-of-the-box / tabletop scenarios for swift mobilisation for future projects, Local Authorities might incentivise responsiveness with business tax breaks, utility discounts, reductions in CIL (community infrastructure levy), etc.

To maximise the site utilisation, I recommend using modular units: whilst starting on phase 1, companies could – permission pending – install modular housing units. This allows site maximisation on one side and creates sales for the developer on the other hand. Initial site-housing might be on termed contracts, i.e., for five years, and allows rapid deployment of excellent timber frames and modular units.

Based on the meanwhile concept, these can move, first within the maturing of the site and, once the site is completed, to a new project altogether. This allows more stock to be available whilst creating a community from the beginning, which helps meet rental demand in the UK.

Close relationships with the Local Authorities will help to ensure a complete understanding of BTR and its differences from other schemes. The main issues currently are space planning, parking[11], and affordability requirements. Reviewing the local framework could result in a more flexible approach to space standards, thus creating more units nationwide. The more openminded the developer and the Local Authority are, the easier and faster changes, such as below, could find their way into the regulatory framework:

The fact that the housing market needs reform is undisputed. Due to the regulatory framework’s complexity and decades of inertia on both sides (local authorities & industry), a new approach to mitigating the steep rental demand across the UK is needed. The industry can work on a regional level with the housing authorities to create a mutual vision and roadmap to pledge swifter and faster results in meeting rental demand in the UK:

[1] BPF: Unlocking Benefits and Potential of Build to Rent, Feb 2017

[2] BPF: Build to Rent Map of the UK, Q1 2020

[3] Ministry of Housing, Communities & Local Government (MHCLG): National Planning Policy Framework, Feb 2019

[4] Ministry of Housing, Communities & Local Government (MHCLG): National Planning Policy Guidance, July 2018

[5] Town and Country Planning Act 1990, Section 92

[6] https://www.theconstructionindex.co.uk/news/view/40-of-houses-with-planning-permission-not-built

[7] BPF: Unlocking Benefits and Potential of Build to Rent, Feb 2017, pg. 48

[8] Successful examples include Barking Riverside Regeneration Project – a cooperation between L&Q and GLA

[9] BPF: Unlocking Benefits and Potential of Build to Rent, Feb 2017, pg. 41

[10] Town and Country Planning Act 1990, Section 56

[11] Transport London, 2012: Residential Parking provision for new developments

MORICON Consultants Limited

Registered Office: Kemp House, 124 City Road, London, EC1V 2NX, UK

Company Reg : 11282307 VAT Reg: 293304896

Copyright © 2017 – 2025

MORICON Consultants Ltd All Rights Reserved

No part of this website may be re-produced or distributed without prior

written permission from the copyright owner.

![]()